블룸버그 프로페셔널 서비스

2024년 8월 2일

작성자: Amine Khanjar, 블룸버그 퀀트 연구원

지금까지 블룸버그 플래그십 채권 지수는 채권 종목의 만기일이 1년 미만이 되면 해당 채권을 즉각 제외해왔다. 초단기 채권 상품은 금리 민감도가 낮으며 일반적으로 신속한 자금 접근성을 선호하는 보수적 성향의 투자자에게 매력적인 옵션이다. 해당 채권의 수익률 추이를 살펴보면 단기금융시장 계정보다는 수익률이 높지만, ‘일반적인’ 상향 일드 커브 환경 속에서의 전통적인 단기 채권보다는 그 수익률이 낮은 모습을 보여왔다.

최근 2022년과 2023년간 중앙은행의 공격적인 긴축기조에 더하여 지난 2년간의 글로벌 일드커브 역전 현상이 지속됨에 따라, 투자자들은 상대적으로 수익률이 좋고, 매력적인 위험 수익률 프로필을 지닌 초단기 채권 종목으로 눈길을 돌리고 있다. 이에 따라, 블룸버그는 만기보유채권(HTM) 지수 및 0-1Y 만기채권 지수를 커버하는 두가지 신규 지수 상품을 출시했다.

만기보유채권(HTM) 지수

신규 HTM지수는 1년 만기 적격성 규정을 제외하고는 플래그십 지수와 동일한 구성 종목 편입 및 제외 규정을 적용한다. 블룸버그 플래그십 채권 지수가 만기가 1년 미만으로 남은 종목을 즉시 제외하는 반면, HTM지수는 실제 만기일이 도래할 때까지 해당 종목을 유지한다. 이로 인해 전반적인 듀레이션을 축소하면서, 매매회전율/거래 비용을 절감할 수 있다. 그동안 1년 만기 한계 조건은 특정 월에 플래그십 지수 내 종목 중 평균적으로 3분의 2의 종목들을 제외시키는 요인이었다.

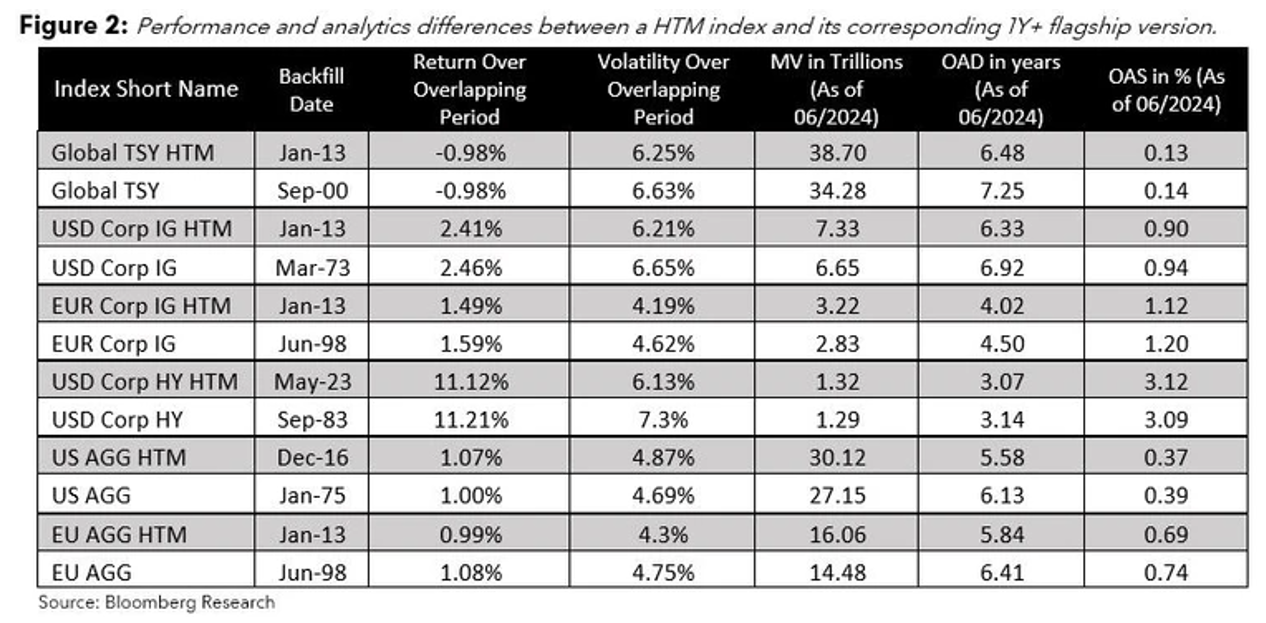

도표 2는 HTM지수와 플래그십 지수가 모두 제공됐던 시기 동안 두 지수 간 시장 가치, 스프레드, 듀레이션 및 수익률 성과에 대한 차이를 보여준다.

HTM 버전의 글로벌 국채지수(헤지하지 않음)는 2024년 6월 28일 기준, 플래그십 글로벌 국채 지수 대비 13%의 시장가치(약 4조 달러) 상회를 기록했다. 듀레이션이 9개월 단축되어 최근 12년간 연간 변동성이 6% 낮아졌다. 2013년 이후 초기에 수익률이 부진했던 시기를 지나 2021년 말 수익률 상회 시기까지 포함하면 두 지수의 통합 수익률은(-1%) 유사한 수준이다. 글로벌 인플레이션 상승에 따른 중앙은행의 급격한 긴축 정책으로 인해 대부분의 선진시장 일드커브가 역전되었다.

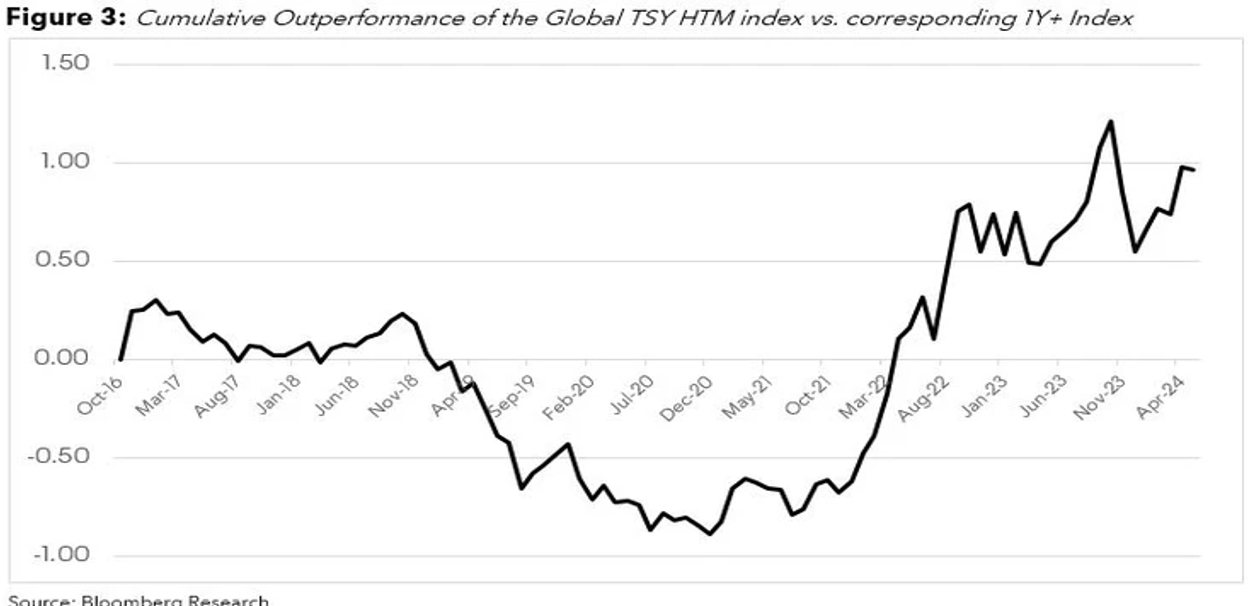

반면, 도표 3에서처럼 HTM버전의 지수는 해당 기간 동안 약 2% 수익률을 상회했다.

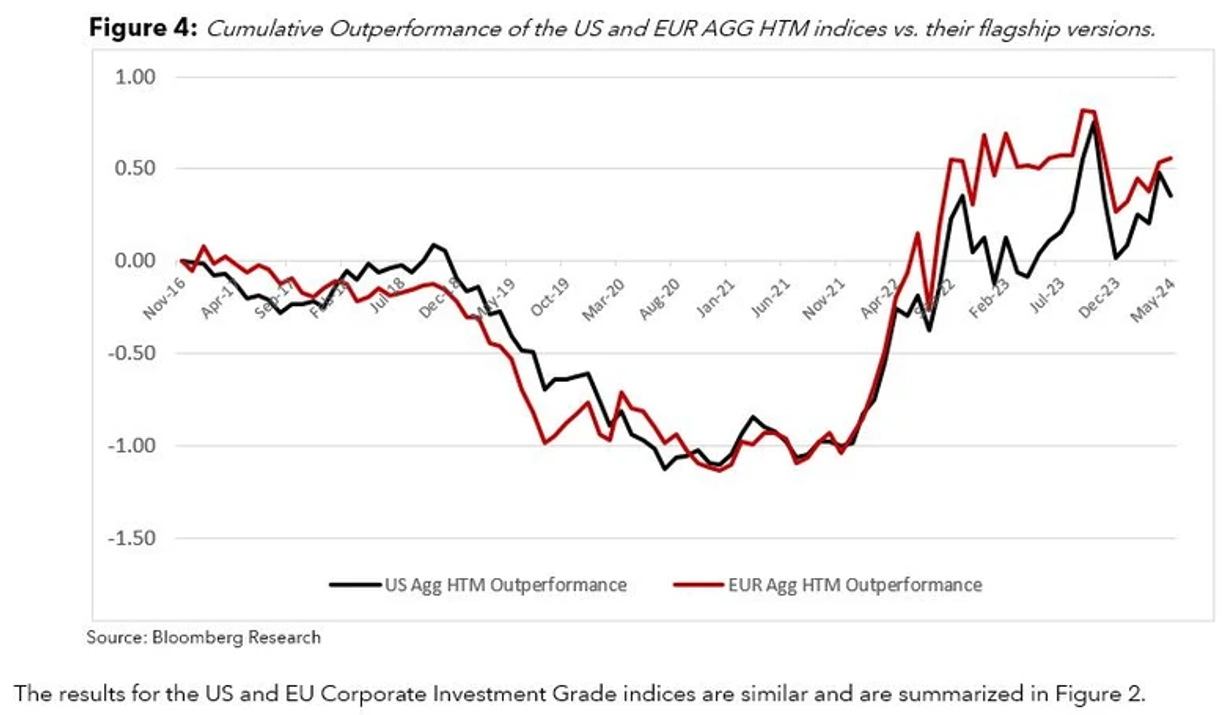

HTM버전의 미국 통합 및 유로 통합 지수는 2024년 6월 28일 기준, 플래그십 지수 대비 11% 시장 가치 상승을 기록했다. 각각의 듀레이션은 모두 6개월 단축되었다.

마찬가지로, 전체 표본기간 동안 2022년 이후 미국 통합 및 유로 통합 지수의 수익률 성과는 각각 1.4%와 1.5% 상회함에 따라 2016-2024년 표본기간동안의 1년 이상 만기 지수 버전과 비교된다.

0-1Y 만기채권 지수

0-1Y 만기채권 지수는 1년 이상 만기 적격성 규정에 부합하지 않아 플래그십 지수에서 제외된 종목으로만 구성된다. 신규 지수군은 월간 재조정을 실시하는 한편, 만기 시점까지 해당 종목을 유지한다. 특정 시점을 기준으로 0-1Y 지수 구성 종목은 HTM 지수와 이에 상응하는 1년 이상 만기 플래그십 지수 구성 종목 간의 차이로 정의될 수 있다.

초단기 채권은 안전성, 유동성 및 수익률 등의 매력적인 조합을 기반으로 균형잡힌 투자 포트폴리오를 구성하는데 중요한 역할을 한다. 초단기 채권에도 위험요소가 있긴 하지만, 최소한의 금리 민감도와 매우 짧은 듀레이션 덕에 자본금 유지 및 단기 재무 니즈 관리를 선호하는 투자자들에게 매력적인 대안이 될 수 있다.

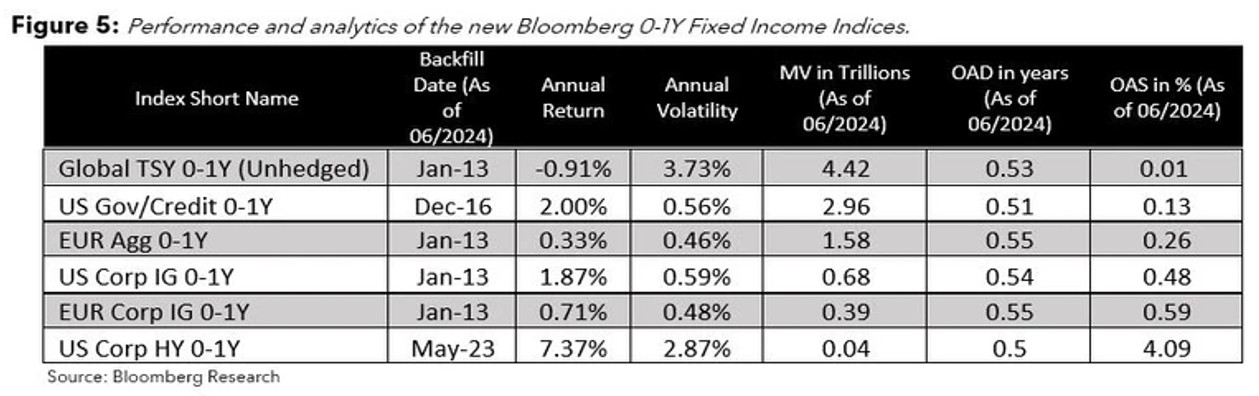

도표 5는 신규 출시된 0-1Y 만기채권 지수군 구성 종목의 시장 가치, 분석 및 수익률 성과를 나타낸다.

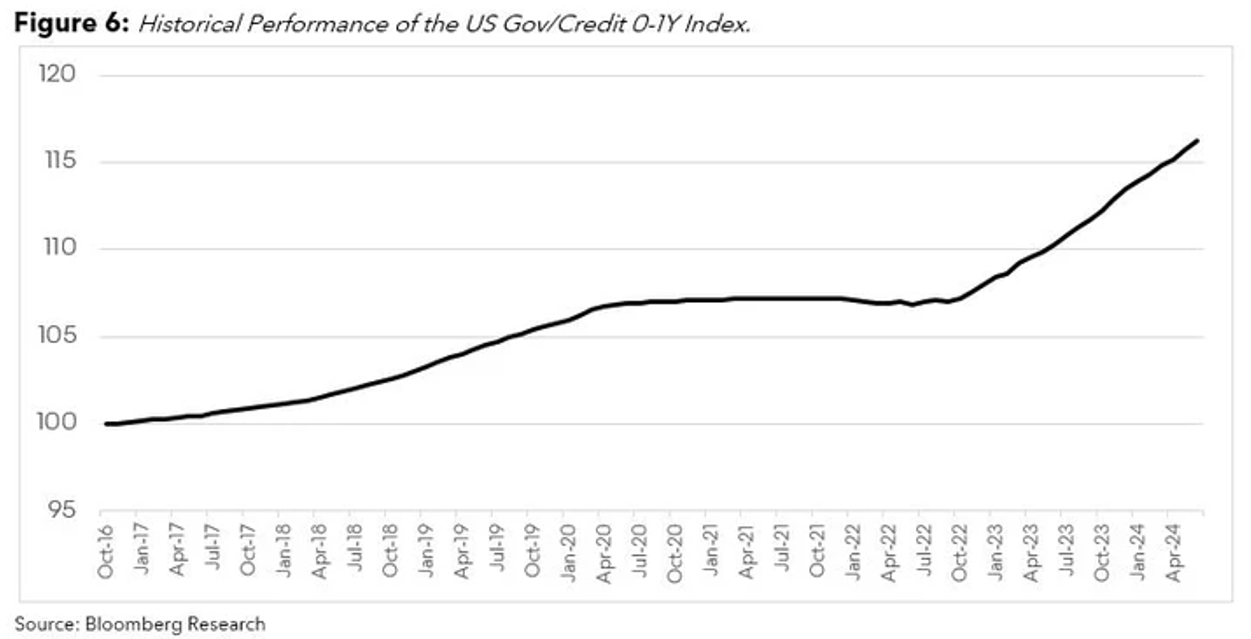

0-1Y 미국채/크레딧 지수의 현재 시장가치는 약 3조 달러 수준이다. 동 지수는 78%의 초단기 국채 및 국채관련 채권과 22%의 투자등급 회사채로 구성된다. 2016년 말 이후 2%의 연간 평균 수익률과 평균 56bp의 연간 변동성을 기록했으며, 평균 듀레이션은 약 6개월이었다.

도표 6은 예상대로 지수 수익률이 중앙은행이 설정한 현행 단기 차입금리와 밀접한 관련이 있음을 시사한다. 2016-2019년 연준금리가 2% 내외였을 당시 지수 수익률은 중간 수준이었으며, 코로나 팬데믹 대응 차원에서 제로금리가 시행되었던 2020년부터 2022년 초까지 지수 수익률은 큰 변동이 없었다. 최근에는 미국 연방준비은행(FRB)이 공격적인 긴축 통화 정책을 추진하면서 지수는 평균 약 4.3% 수익률을 기록했다.

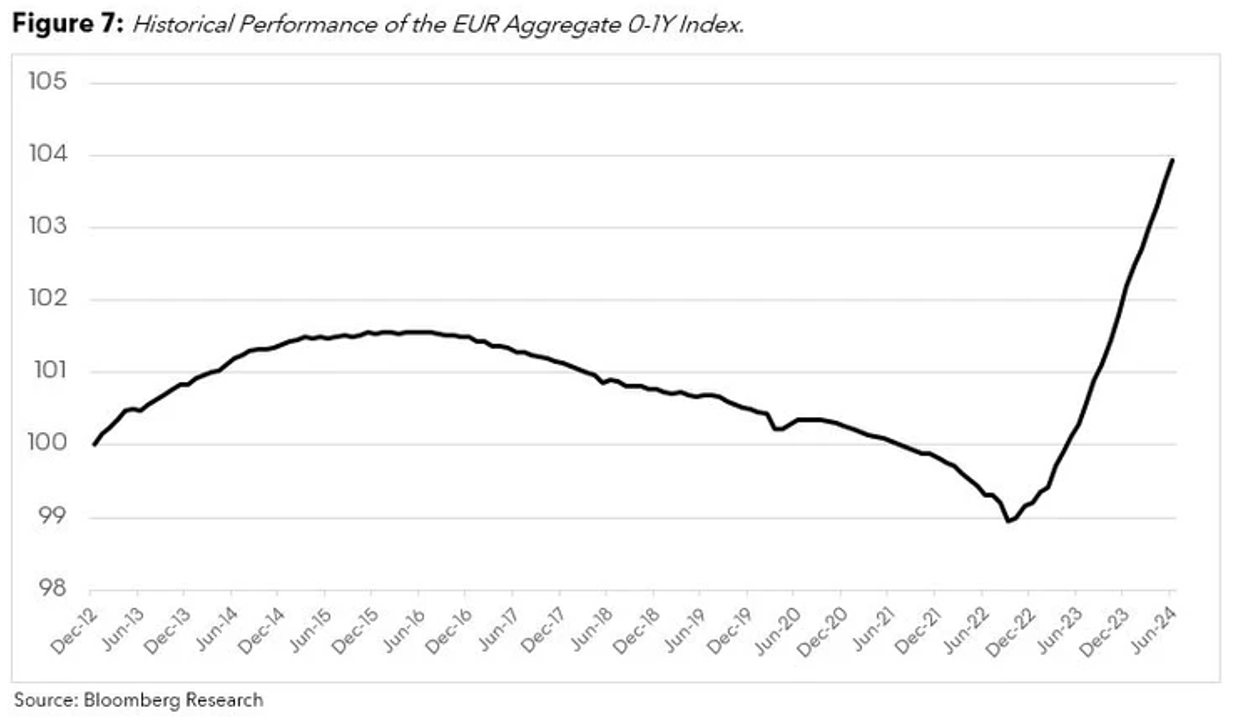

한편, 0-1Y 유로 통합 지수는 2024년 6월 28일 기준 1조 6천억 유로의 시장 가치를 보유하고 있다. 동 지수는 66%의 초단기 국채 및 국채 관련 채권과 33%의 투자등급 유로 회사채로 구성되며, 2013년 말 이후 33bp의 연간 평균 수익률과 평균 46bp의 연간 변동성을 기록했다.

도표 7은 0-1Y 유로 통합 지수의 수익률 성과 패턴도 비슷함을 보여준다. 유럽 단기 차입금리가 마이너스였던 2017-2022년 당시 지수 수익률은 마이너스를 기록했다. 최근 2년동안은 유럽중앙은행 역시 긴축 통화정책을 시행함에 따라 지수는 평균 약 2.4%의 수익률을 나타냈다.

Bloomberg does not represent that the quantitative models, analytic tools and/or other information (“Content”) referenced in this publication (including information obtained from third party sources) is accurate, complete or error free, and it should not be relied upon as such, nor does Bloomberg guarantee the timeliness, reliability, performance, continued availability, or currency of any Content. The Content is provided for informational purposes only and is made available “as is.” Because of the possibility of human and mechanical errors as well as other factors, Bloomberg accepts no responsibility or liability for any errors or omissions in the Content (including but not limited to the output of any quantitative model or analytic tool). Any data on past performance, modelling or back-testing contained in the Content is no indication as to future performance. No representation is made as to the reasonableness of the assumptions made within or the accuracy or completeness of any modelling or back-testing.

Bloomberg shall not be liable for any damages, including without limitation, any special, punitive, indirect, incidental, or consequential damages, or any lost profits, arising from the use of or reliance on any Content, even if advised of the possibility of such damages.

The Content (including any of the output derived from any analytic tools or models) is not intended to predict actual results, which may differ substantially from those reflected.

Information and publications provided by Bloomberg shall not constitute, nor be construed as, investment advice or investment recommendations (i.e., recommendations as to whether to “buy”, “sell”, “hold”, or to enter or not to enter into any other transaction involving any specific interest) or a recommendation as to an investment or other strategy. No aspect of the Bloomberg publications is based on the consideration of a customer’s individual circumstances. Information provided in the publications should not be considered as information sufficient upon which to base an investment decision. You should determine on your own whether you agree with the conclusions made in the publications.

Bloomberg offers its services in compliance with applicable laws and regulations. Services and information provided by Bloomberg should not be construed as tax or accounting advice or as a service designed to facilitate any subscriber’s compliance with its tax, accounting, or other legal obligations. Employees involved in Bloomberg may hold positions in the securities analysed or discussed in Bloomberg publications.

This publication has been distributed by Bloomberg. “Bloomberg” means Bloomberg Finance L.P., Bloomberg L.P., and their affiliates.

© 2024 Bloomberg. All rights reserved.